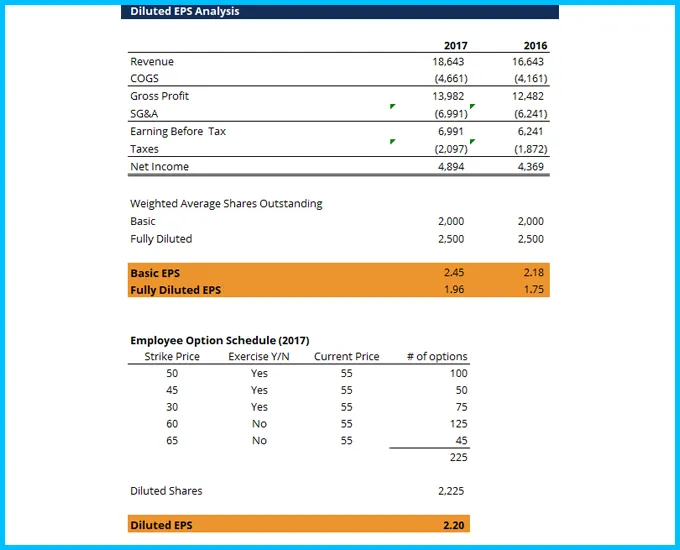

This Diluted EPS Formula template shows you how to compute the diluted earnings per share using information from the income statement and an employee option schedule.

The Diluted EPS formula is equal to Net Income less preferred dividends, divided by the total number of diluted shares outstanding (basic shares outstanding plus the exercise of in-the-money options, warrants, and other dilutive securities).

Diluted EPS Formula:

Diluted EPS = (net income – preferred dividends) / (weighted average number of shares outstanding + the conversion of any in-the-money options, warrants, and other dilutive securities)

The reason that analysts and investors calculate diluted EPS is that basic EPS may overstate the actual amount of earnings per share that a common shareholder is entitled to.

Companies frequently have dilutive securities outstanding – like options and warrants – that will increase the total number of shares outstanding when converted.

Since the conversion of options into shares won’t add any additional net income to the business, the increased share count makes the conversion dilutive.

Options may have been granted to employees, for example, that are in-the-money (strike price is below the current market price) but have not been converted yet. If options are in-the-money, they should be accounted for in a diluted EPS calculation.

Credits to : Corporate Finance Institute

Test Template John Doe 888

Leadership Slide Template for PowerPoint

Test Template John Doe 888

Leadership Slide Template for PowerPoint

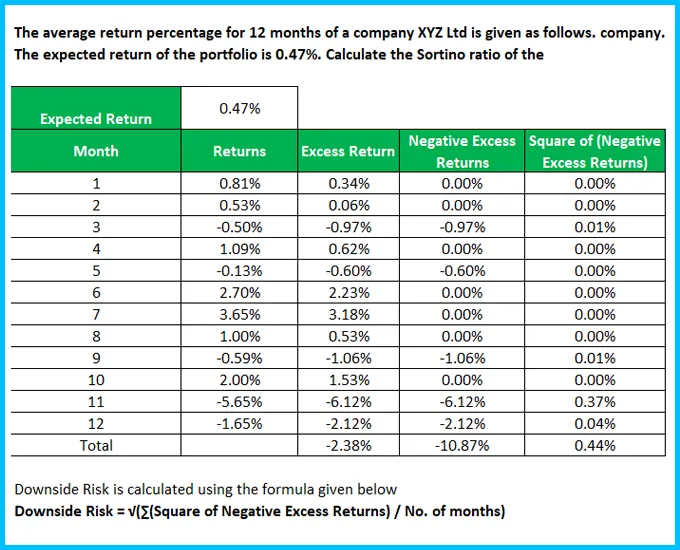

Sortino Ratio Template

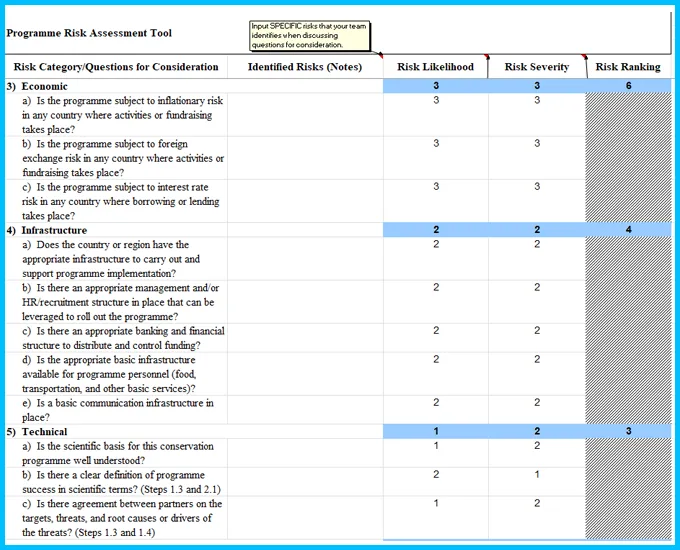

Risk Ranking and Mitigation

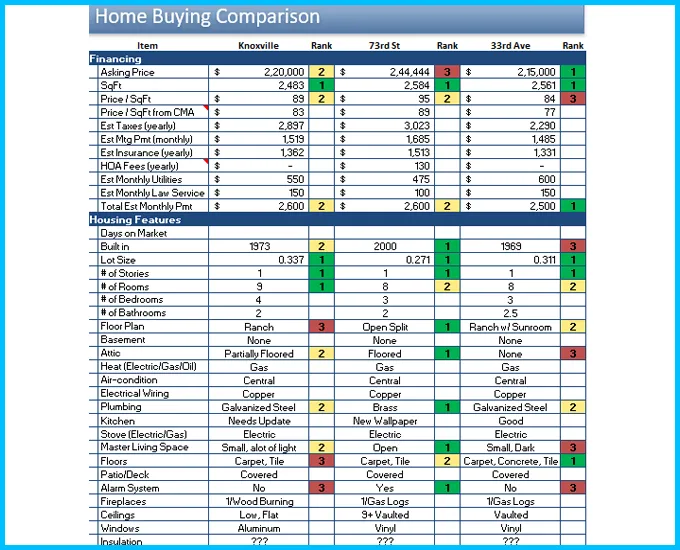

Home Buying Comparison Template

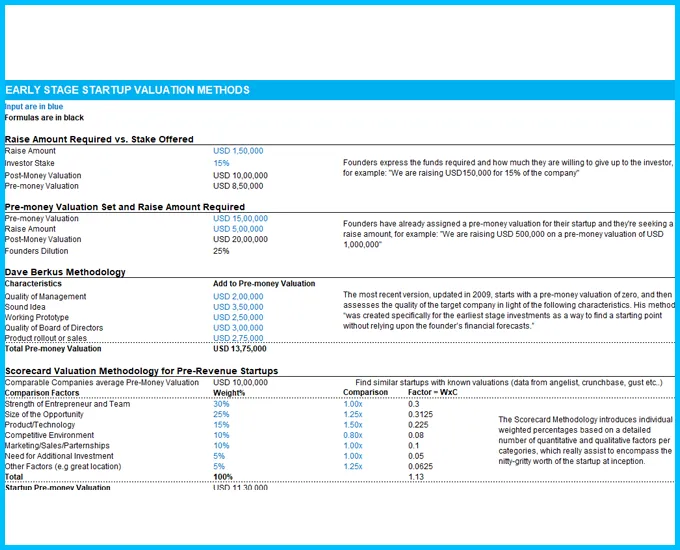

Early Stage Startup Valuation Methods

Commercial Real Estate Valuation Model

Checkbook Register Template

Sortino Ratio Template

Risk Ranking and Mitigation

Home Buying Comparison Template

Early Stage Startup Valuation Methods

Commercial Real Estate Valuation Model

Checkbook Register Template

Project Management Agreement Template

Wedding photography contract Template

Non Disclosure Agreement Template

Event Budget Template

Cold Email Sales Weekly Activity Spreadsheet

Branding and Creative Budget Template

Blog Editorial Calendar - Google Calendar

Project Management Agreement Template

Wedding photography contract Template

Non Disclosure Agreement Template

Event Budget Template

Cold Email Sales Weekly Activity Spreadsheet

Branding and Creative Budget Template

Blog Editorial Calendar - Google Calendar

Find a pre-made digital template of any type and topic or ask a professional to create a custom one for you